WHAT’S HAPPENING?

HMRC are aiming to simplify the rules for unincorporated businesses by applying basis periods so that company profits are calculated in line with the usual tax year (6 April to 5 April each year). This could lead to some individuals facing larger tax bills than expected.

WHEN WILL THIS HAPPEN?

The transition to the new system would begin in 2022/23 and the changes would be fully effective from the 2023/24 tax year.

WHO WILL BE AFFECTED?

Unincorporated businesses such as sole traders (self-employed individuals), partnerships, trusts and estates who use a tax year other than 5 April.

WHAT ARE THE NEW RULES?

Currently, self-employed individuals, sole traders and partnerships are taxed on their accounts ending in the tax year. Going forward, the reform means that they would instead be taxed on profits arising within the same 12 months as the tax year, with the intention of aligning the way self-employed profits are taxed with other forms of income.

The aim is to align the way in which individuals’ income is taxed, reduce the time spent by small businesses filling out their taxes, make the rules fairer, more logical, and easier to understand.

It’s likely that the changes will enable the introduction of Making Tax Digital for non-company businesses from April 2023. This would involve the submission of a quarterly return showing taxable profits to HMRC. The basis period reform will allow these quarterly submissions to align with the correct tax period.

HERE’S AN EXAMPLE:

Under the current rules, a business with a year end of 30 September 2021 would be taxed on these profits in the tax year to 5 April 2022. Under the proposed changes, the business will now be taxed on the profits accumulated from 6 April 2021 to 5 April 2022.

If, as a result of the transition, a business has any profits which are taxed twice in separate tax years, then the ‘overlap profits’ from the earlier year of trade are to be deducted as a relief from the profits of the transitional year.

For businesses where profits in the transition tax year are higher than if calculated under the current basis of assessment, because of the changes to basis periods, the Government proposes an election to spread any ‘excess profits’ in the transition year over up to five years.

WHO ARE THE WINNERS & LOSERS?

Those with a year end date of 31 March or 5 April will see no change as a result of the reform.

Those with different year end dates will need to apportion their profits over a couple of accounting periods to determine their individual tax liability for the year. This could involve including estimates if their accounts are yet to be finalised, thus creating a likely admin burden if the actual results differ from the estimates provided to HMRC.

In the long run, should the process be as simple as HMRC hope, then it could be a positive change.

Check out the below examples for how it might affect you…

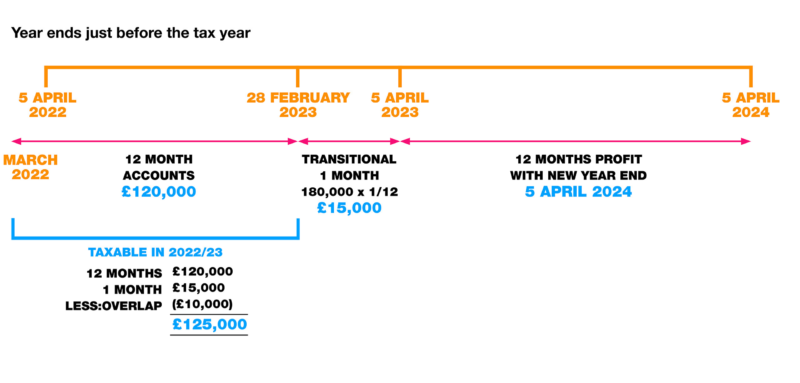

WINNERS

Let’s assume a sole trader has a year-end date of 28 February and records profits of £120,000 in year one, and £180,000 in year two. They also have overlap profits brought forward of £10,000.

Usually, they would pay tax on their taxable profits using the current year basis method, so the 12 months to 28 February each year. In this example, £120,000 for the year to 28 February 2023.

However, after the change in rules, for the transitional year, they will be taxable on the profits for the full year to 28 February 2023 and 1/12 of the following year profits to bring them in line with a 5 April 2023 year end. Thus, making the total taxable profits for the year £125,000 after deducting the overlap profits.

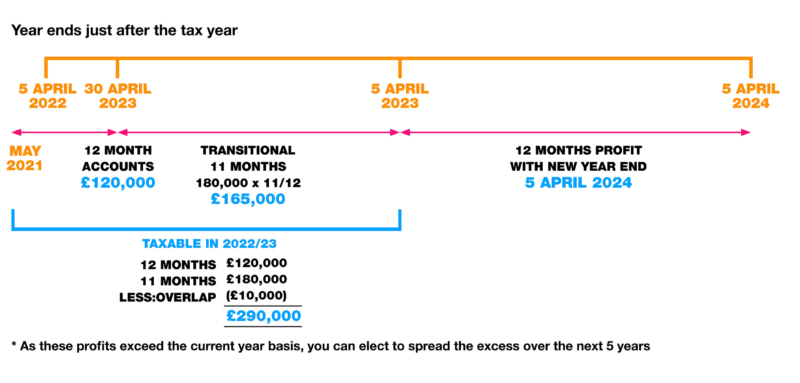

LOSERS

LOSERS

Here, we’ll use the same example, with profits of £120,000 in year one, £180,000 in year two and overlap profits of £10,000, but this time with a year end of 30 April.

You would instead be taxable on the full 12 months of taxable profits from year one for the accounts to 30 April 2022, and then 11/12 of profits from year two to bring the accounts up to 5 April 2023 and in line with the tax year going forward.

SO, WHAT CAN YOU DO?

SO, WHAT CAN YOU DO?

If you have any concerns about the impact of this reform on yourself or your business, then please feel free to get it touch.

Our Private Client and Business Tax teams will be happy to help you with any queries or advice needed on the reform, so you can simplify your tax compliance responsibilities.